Tackling non-financial misconduct in financial services

Did the FCA seize the opportunity to finalise its position?

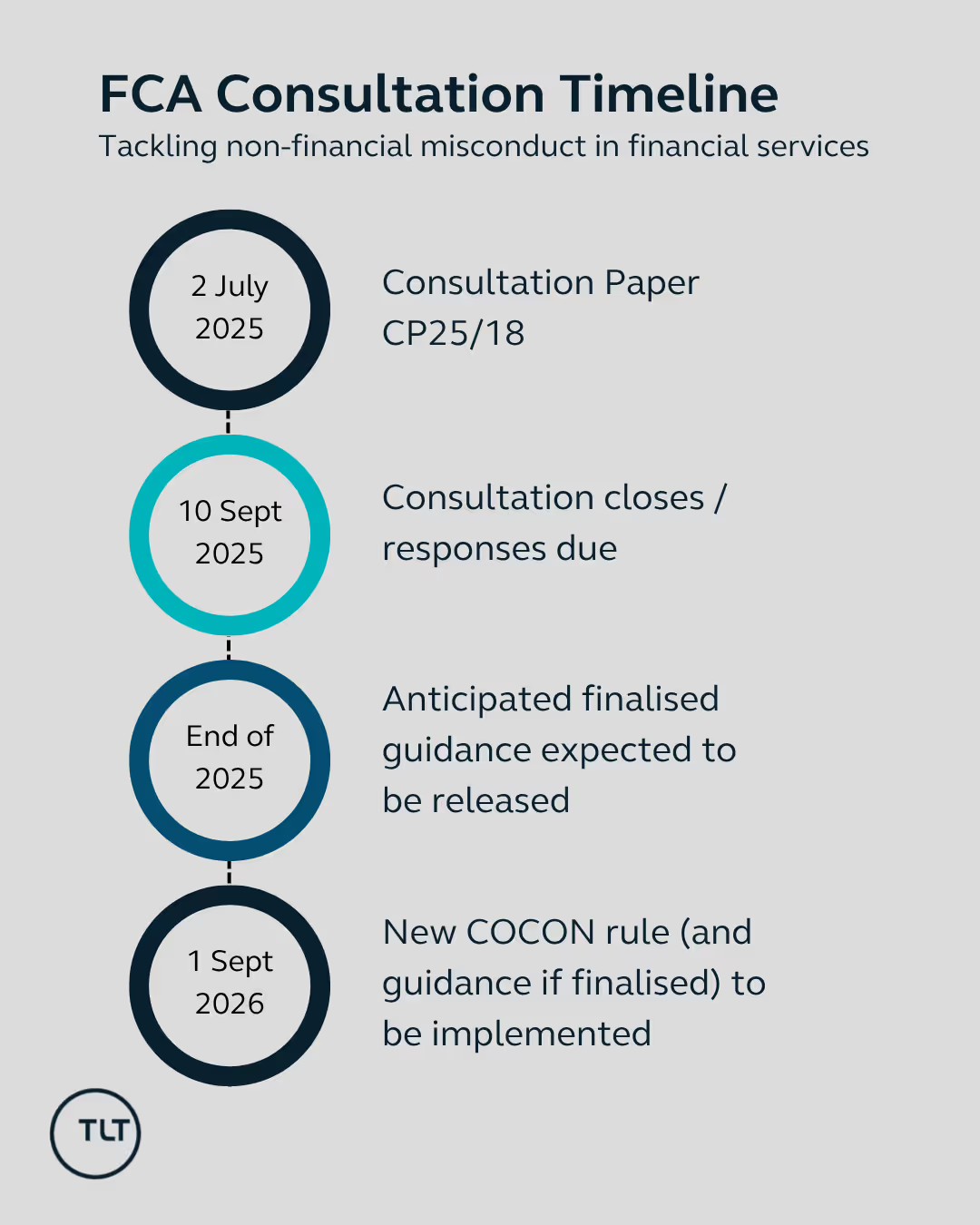

On 2 July 2025, the FCA launched a consultation on draft guidance aimed at supporting firms dealing with non-financial misconduct (NFM). It also published a Policy Statement confirming final rules in the Code of Conduct sourcebook (COCON) that extend existing NFM rules to non-banks.

This article considers the changes, the proposed draft guidance and what firms should do now.

(1) Extension of existing NFM rules to non-banks

The Policy Statement changes the rules governing the scope of COCON to capture serious NFM (defined – for the purposes of COCON – as bullying, harassment and violence against a fellow member of the workforce) within non-banking firms (such as financial advisors and asset and fund managers).

The new rules will come into effect from 1 September 2026. This date aligns with the existing conduct rule breach reporting period applicable to most firms and allows time for the FCA to finalise any accompanying guidance. The new rules will not apply retrospectively and there is no expectation of any retrospective analysis as to whether a past conduct rule breach has been correctly determined. However, the treatment of past behaviour that only comes to light after 1 September 2026 is unclear.

In response to feedback, the definition of NFM covered by the new rule is aligned with the definition of similar conduct under employment law, particularly the definition of harassment (in section 26 of the Equality Act 2010). Both require unwanted conduct to have the purpose or effect of: (i) violating dignity; or (ii) creating an intimidating, hostile, degrading, humiliating or offensive environment. The FCA flags that this should assist interpretation and application of the rule. However, it is important to note that, unlike the Equality Act 2010 definition of harassment, conduct under the new rule does not have to be related to a “relevant protected characteristic”, and therefore potentially catches a wider range of workplace misconduct, reflecting the fact that a wide range of workplace misconduct is relevant to the FCA’s statutory objectives.

(2) Consultation on draft handbook guidance

The FCA has set out proposals for potential new Handbook guidance in COCON and the Fit and Proper test for Employees and Senior Personnel sourcebook (FIT), reflecting feedback on previous draft guidance consulted on in CP23/20. It confirmed that it is not taking forward its proposals for guidance on Suitability under the FCA’s Threshold Conditions or the giving of regulatory references.

The FCA states that the purpose of the proposed guidance is to make it easier for firms to interpret and consistently apply the conduct rules, and to clarify statutory and FCA requirements for fitness and proprietary.

The consultation on the proposed guidance is open until 10 September 2025. The FCA states that it plans to review the feedback and set out its final regulatory approach before the end of this year, so that firms have good time to update their processes prior to the rule implementation date.

Whilst the FCA has said that it will “only proceed with the guidance if there is clear support for it”, we anticipate that this support will be readily forthcoming in an industry that has been calling out for more clarity and consistency on NFM assessments for years.

We examine the proposed guidance in more detail below.

Helpfully, the draft guidance clarifies that COCON does not apply to behaviour in personal or private life. It also includes examples to help firms judge the boundary between work and personal conduct and explains when behaviour falls outside of SMCR financial activities. It also confirms that conduct isn’t excluded from the scope of COCON just because it is banned by a firm’s own internal policies, or is harmful to a firm.

The proposed guidance seeks to clarify when bullying, harassment or violence may fall outside of the scope of COCON for non-banks, namely when behaviour clearly relates only to a part of the business that doesn’t carry on regulated or SMCR financial activities. To bring this to life, an example is provided where a firm separates its HR function into those dealing with staff in the financial service business and those dealing with staff in other parts of the business, confirming that the latter may fall outside the scope of COCON. Looking ahead, some firms may consider staff segregation to avoid the application of COCON, albeit behaviour such as bullying, harassment or violence would of course be likely to be caught under employment law in any event.

The guidance also gives some helpful clarity on the factors to consider when determining whether NFM breaches the conduct rules.

Firstly, it clarifies that subjecting a colleague to detriment for disclosing information to regulators or for using the firm’s whistleblowing procedures, would be a breach of Individual Conduct Rule 1 (‘you must act with integrity’). This is unsurprising given the importance the FCA places on culture and psychological safety. This approach also aligns with rules around victimisation under employment law.

Secondly, it sets out the factors to consider when deciding if NFM breaches either Individual Conduct Rule 1 or Individual Conduct Rule 2 (‘you must act with due skill, care and diligence’). Factors to consider include:

1.Whether the NFM is ‘serious’, which might be the case depending on the repetition, duration and impact of conduct (which may involve looking at later actions as well), the seniority and vulnerabilities of those involved, and whether there have been prior warnings or criminality. This concept of ‘serious’ broadly aligns with the concept of ‘serious’ in the SRA sexual misconduct guidance, which the FCA has previously drawn on (see our previous insight), and which might be familiar to firms. It differs however to the concept of ‘serious’ in the FIT guidance – see below – which makes navigation of the various tests tricker for firms.

2.“All the circumstances of the case” which seems to include both a subjective and objective element being (i) the perception of the subject of the misconduct (e.g. if the subject didn’t perceive their dignity to be violated, there is no breach) and (ii) whether it was reasonable for the conduct to have the perceived effect (e.g. if it wasn’t reasonable, there is no breach). However, what is not clear is how firms should balance the subjective and objective elements of this test, and it may be prudent to take advice on this point, particularly as this overlaps with the test for harassment under employment law and so lessons may meaningfully be taken from that sphere.

3. Conduct may fall under COCON whether it’s a single act, repeated incidents, or ongoing behaviour, and can include physical violence as well as words, gestures, or communications.

However, both Rule 1 and Rule 2 also have additional and specific thresholds which may mean that NFM falls outside the scope of those rules:

Rule 1 requires a lack of integrity (i.e. behaviour that is deliberate or reckless). NFM may therefore fall outside its scope if the staff member reasonably believed their actions were justified and proportionate or if the staff member did not intend to cause harm and were not reckless about the effect of the conduct (although repeated behaviour would make it more likely they intended or knew of the harm).

- Rule 2 requires a lack of due skill, care and diligence. NFM may therefore fall outside its scope if the staff member thought the conduct would have no ill effects and a reasonable person with the same skills would have thought the same and thought the conduct was justified.

The addition of this subjective element to the COCON test enables sufficient regard to context and reasonableness, which is welcome given that adverse findings have the potential to severely impact an individual’s career and livelihood.

The practical effect is that NFM will more likely be captured by Rule 2 than Rule 1 given the threshold in relation to Rule 1 is higher and has more subjective elements. In light of this, it may be that the seriousness test is more of a determining factor in relation to Rule 2.

Finally, it should be noted that the guidance gives some helpful examples of reasonable steps for senior managers to protect staff against NFM and flags that there will not be in breach of Individual Conduct Rule 2 if managers have acted reasonably. HR functions and senior managers should review these, particularly in light of the recent and upcoming changes to the duty to prevent sexual harassment.

The draft guidance explains how conduct, including NFM, forms part of the fit and proper test in FIT.

It makes clear that each assessment should be on a case by case basis and should include relevant factors such as the seriousness of the breach (the assessment of which differs to that under COCON, and seems to be broader than that of the SRA in its sexual misconduct guidance), timing of the breach, steps to address behaviours/competence issues/rehabilitation, remorse, absence of mitigating factors, past record, health and life events that might cause out of character behaviour, repetition and likelihood of recurrence, seniority and relevance of the breach to role. In this respect the list of mitigating factors is wider than that of the SRA.

It also gives clear guidance that, whilst COCON is limited to conduct related to a firm’s activities (and sometimes only to a part of its activities) an assessment of fitness and propriety should not be limited in that way; relevant conduct may occur outside work. The guidance on proximity here takes a similar approach to the SRA’s sexual misconduct guidance. Some key points:

It specifically gives the example of violence or sexual misconduct against an individual in their private or personal life and explains that this might show there’s a risk of similar misconduct in relation to customers or counterparties or people in the firm and so is relevant.

It states that breaches of law that would not otherwise be relevant might be relevant where repeated – for example, a minor driving offence might be relevant if frequently repeated.

- It explains that, even if there is no risk of misconduct in a person’s private life being repeated in their work for a firm, it may be relevant if it demonstrates a willingness to disregard ethical/legal obligations, abuse a position of trust or exploit the vulnerabilities of others, and/or it is sufficiently serious that it could undermine public confidence in the regulatory system/impact the FCA’s objectives.

The guidance also flags that generally a firm need not monitor the private lives of its staff subject to FIT; they need only look at private life if there a good reason to (such as an allegation being brought to their attention).

In these circumstances, whilst the FCA recognise that a firm will normally rely on formal findings (such as court findings) to assess whether wrongdoing in private life has taken place, a firm should nevertheless consider what steps it can reasonably take to assess the possible impact on fitness and propriety. Firms might, for example, ask for an explanation from the member of staff.

Helpfully, the guidance also clarifies the FCA’s approach to NFM on social media, noting that social media activity may be relevant to fitness and proprietary where it indicates a real risk that the person will breach the requirements and standards of the regulatory system. However there also seems to be an acknowledgement that social media is a grey and developing area, and that there is a balance to be had (as in employment law) between regulatory concepts and the laws relating to freedom of speech and expression. Indeed, the guidance specifically states that a person can lawfully express views on social media even if they are controversial or offensive without calling into question their fitness under FIT, even if colleagues are upset by those views.

Finally, the guidance makes clear that findings of bullying, harassment, victimisation or discrimination – whether by a tribunal, court, or upheld internal complaint – should be considered when assessing fitness and propriety. This will require FIT assessments to be aligned with HR processes, to ensure that any such findings are captured and considered.

(3) Our thoughts and Next steps

After more than seven years of focus on NFM, firms may be frustrated that the FCA has opted for another consultation rather than finalising its guidance. This likely reflects the regulator’s attempt to balance clarity and consistency for firms with its broader aim of reducing regulatory burden.

Still, there are positives. The proposed guidance brings us closer to understanding the FCA’s expectations. It confirms that private life is only relevant to fitness and propriety, offers examples to help firms navigate the work/personal boundary, and makes clear that firms aren’t expected to monitor employees’ private lives. It also introduces a subjective element to NFM assessments, acknowledges the importance of context, and outlines reasonable steps managers can take to prevent harassment without triggering a breach of Individual Conduct Rule 2. Of course, firms also have another chance to shape the final version of the guidance by responding to the consultation.

However, challenges remain. Firms will need to: navigate inconsistent thresholds across FCA, employment, and disciplinary frameworks; balance subjective and objective elements in NFM assessments; and interpret varying definitions of “serious / significant” across conduct rules, fitness and propriety, reporting, and references. Whilst it is clear that the new rules on scope for non-banks won’t have retrospective effect, it’s not yet clear how past behaviour should be treated where it comes to light after changes are implemented. There are therefore still a number of unanswered questions.

So, what should firms do now?

- The consultation on the draft guidance will be open for 10 weeks until 10 September 2025. Firms should digest the consultation and consider whether they want to respond.

- If your firm is a non-bank, review the new rule in COCON which expands the scope to cover non-banks, consider what changes you may need to make to any relevant policies and procedures and what training staff might require.

- For both bank or non-bank firms, consider whether any changes will be required to your policies and procedures to reflect the guidance ahead of the anticipated 2026 implementation date. Whilst there is a chance that it will be dropped, the guidance reflects what the FCA currently considers to be best practice and so it would be advisable to have regard to the key points when assessing regulatory matters. HR, legal and compliance should be fully aware of the guidance and should ensure they are aligned.

- Diarise the key dates on our timeline below.

Please get in touch if you would like any assistance in responding to the consultation, updating or adapting your policies and procedures or creating training. Our team would also be very happy to answer any questions you might have on the above, or the possible impact on your firm.

Co-author: Catherine Roylance

This publication is intended for general guidance and represents our understanding of the relevant law and practice as at July 2025. Specific advice should be sought for specific cases. For more information see our terms and conditions.

Get in touch

%20%C3%94%C3%87%C3%B4%20790px%20X%20451px%2072ppi10.jpg)

Get in touch

Insights & events

FCA raises the bar on Consumer Duty outcomes monitoring: what your firm needs to do now

Inside the minds of money mules: what new Home Office research means for your anti-financial crime framework

FCA updates complaints and root cause analysis good practice guidance – what firms need to know

FCA product governance review: what firms must do now to get product design right under Consumer Duty

Payroll providers and HMRC AML supervision: why registration is the easy part

Consumer Duty enforcement is here – 11 investigations and counting

Lenders successful in judicial review of the Financial Ombudsman Service

FCA publishes landmark Mills Review into AI and retail financial services: what firms need to know

Consumer Duty: Distribution chains, manufacturer obligations and board reporting – what firms need to know

Senior exits in a post-cap world: Managing employer risk following unfair dismissal reforms

What the first three OFSI Settlements tell us about UK sanctions enforcement

FCA flags financial crime control gaps across insurance sector in new multi-firm review

Government announces once-in-a-generation overhaul of the home buying and selling system

Quarterly update on Northern Ireland employment law October 2022

10 Key Points from the PSR Consultation APP Scams: Requiring reimbursement

Quarterly update on Northern Ireland employment law June 2022

Quarterly update on Northern Ireland Employment Law December 2021

Quarterly update on Northern Ireland employment law June 2021

TLT Advises on Funding for Irish Solar Projects | TLT

TLT turbocharges UK-wide Banking team with high-profile partner hire

TLT continues growth of financial services regulatory team with appointment of new partner

TLT advises administrators appointed to rescue iconic Typhoo Tea

TLT bolsters employment expertise with legal director hire in Belfast

TLT advises Allied Irish Bank on completion of refinancing investment facility

TLT strengthens employment team with new partner hire in Birmingham

TLT strengthens banking team with recruitment of Scottish banking heavyweight

TLT advises renewable energy company on funding partnership

TLT continues expansion of future energy team with appointment of regulatory expert

Ainslie Benzie named Finance Rising Star of the Year at The Legal 500 Scotland Awards

TLT grows future energy team with project finance partner hire

TLT shortlisted for two awards at Manchester Legal Awards

TLT bolsters structured finance practice with second partner appointment in four months

TLT completes acquisition of UK bank for US-based global digital home ownership platform

Employment Law Focus - Understanding the Neonatal Care (Leave and Pay) Act 2023

Employment Law Focus flexible working and the four day work week

Employment Law Focus: The impact of AI on employment law

Employment law focus - Winter 2022 and the cost of living crisis

Employment law focus: An update on gender equality issues at work

The rise of the disability agenda - Employment Law Focus - episode thirteen

Views on fintech - interview with Niels Pedersen, MMU

UK Utilities Case Study: Employment Law and Brexit Planning | TLT

Bitesize ERA - Episode 7: Modernising trade union ballots under the ERA reforms

Bitesize ERA - Episode 6: Delivering change under the ERA reforms

Alternatives to redundancy for the leisure, food and drink sector