M&A Market Monitor 2025

Understanding deal trends and opportunities

M&A activity in the UK has experienced fluctuations over the past two years, influenced by economic, political, and global uncertainties.

Deal activity began to stabilise in the second half of 2024, and there was a surge in transactions completing ahead of the Autumn Budget, driven by anticipated capital gains tax increases. M&A transactions are picking up momentum, with growth in sectors such as Financial Services, Healthcare, Artificial Intelligence, Technology and Construction. Transactions in Future Energy and involving an Employee Ownership Trust model also remain robust and dynamic.

The TLT M&A Market Monitor contains detailed analysis of 59 transactions completed over the past two years by our Corporate team across England and Scotland, providing valuable data and insights into the current state and future direction of the UK M&A market.

Business leaders, investors and stakeholders can use this report to make informed decisions and capitalise on emerging opportunities.

Download the M&A Market Monitor 2025

In the report

There is cautious optimism that the stabilisation of interest rates and inflation alongside greater political stability will boost M&A activity in the UK. Financial Services, AI, Technology and Healthcare are expected to continue to be popular sectors for buyers seeking growth opportunities.

Pricing mechanisms have shifted, with an increased use of locked box methods, indicating a potentially improving market for sellers. Deferred consideration has seen reduced use, while retentions are utilised less frequently due to the burdens of formal escrow arrangements.

Increasingly used to bridge valuation gaps, with two thirds lasting two years or less. EBITDA remained the primary metric, although earn-outs based on specific products or service lines rose. Unspecified earn-out values and periods over five years also increased, reflecting longer-term integration plans and giving sellers longer to maximise potential returns.

Warranty and indemnity (W&I) insurance remains important, offering sellers a clean exit and buyers broader protection. Buyers are carrying out extensive due diligence to ensure a comprehensive understanding of the target business and verify pricing, with a strong emphasis on regulatory and ESG matters. This is impacting deal timelines.

Merger clearance controls and regulatory approvals are becoming more prevalent. Nearly half of Financial Services deals required regulatory approval, achieved within six months on average. This impacts completion timelines and often results in warranties being provided at exchange and completion, with termination rights for breaches, material adverse changes or tax covenant violations.

Crucial in negotiations, they address competition, branding, and interactions with the target company’s employees, customers, and suppliers. Typically, they last two to three years after completion, but there has been an uptick in longer durations which corresponds with longer earn-outs. Ensuring they are proportionate and not anti-competitive is essential.

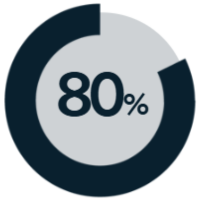

Pricing mechanism

80% of deals employed some form of pricing mechanism, with locked box representing 34%.

Earn-outs

Earn-outs featured in 59% of deals helping to balance the valuation expectations of buyers and sellers in an uncertain economic outlook.

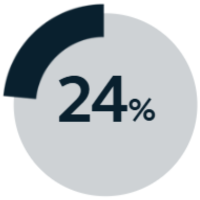

Exchange-completion gap

Greater number of deals with a gap between exchange and completion (24%) due to regulatory landscape and third-party consents.

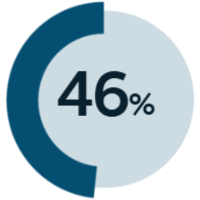

Regulatory approval

46% of deals in the FS sector required regulatory approval.

Overseas entities

Reduced number of deals involving overseas entities (25%).

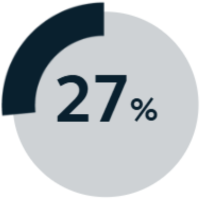

Deferred consideration

Number of deals involving some form of deferred consideration has decreased (27%).

Get in touch

%20%C3%94%C3%87%C3%B4%20790px%20X%20451px%2072ppi10.jpg)

Get in touch

Insights & events

EU Court ruling on loan servicing fees: a VAT wake-up call for securitisation structures?

Why an Employee Ownership Trust could be the right exit for your business

UK withholding tax – a renewed risk focus for borrowers in cross-border financings

UK-India Social Security Agreement – What employers need to know ahead of Summer 2026

When the technical advice is right but still not enough: the role of tax governance

The UK Carbon Border Adjustment Mechanism and potential impacts on projects

Sun, sea… and tax risk? What boards need to know about working abroad this summer

Umbrella company reform: what businesses need to do now

Tax in the Financial Services Sector 2025: Dealing with historic tax issues

The role of lenders in the transition to employee ownership

Employee Ownership - How an EOT can support your ESG agenda

Standish v Standish - Supreme Court ruling on matrimonial assets

Tax in the Financial Services Sector 2025 - the Temporary Repatriation Facility

Guide to the UK Government proposed reforms to the corporate insolvency regime

TLT consolidates national corporate strength with new Partner appointment

TLT advises Dalmore Capital on acquisition of seven river hydropower sites

TLT advises K3 Capital Group on investment into two financial advisory firms

TLT acts for Pollen Street Capital on acquisition of Leonard Curtis

TLT advises shareholders of ABEC on sale to Magnesium

TLT advises Praetura Ventures on funding for sustainable manufacturing start-up

TLT enhances corporate practice with appointment of new partner

TLT amongst finalists at Legal 500 ESG Awards 2025

TLT assists pioneering clinical-stage diagnostics company on investment

TLT advises UK shareholders of Barry‚ in connection with the private equity investment by Princeton Equity Group

TLT advises Innova on sale of Stokeford Solar Farm to global renewable infrastructure managers

TLT acts for Northwest startup businesses on landmark investment

TLT completes sale of Inside Travel Group to new investors

TLT advises leading UK and Ireland tour operator on its transition to employee ownership

TLT advises Sortera on acquisition of Reston Waste Management

World View: The International M&A podcast episode five

World View: The International M and A podcast - Episode four

Scale-up Insights - episode one - the funding landscape

TLT oversees an international acquisition of a specialised South West business

TLT advises on the £90m sale of long-standing client's business

Advising a fast-growth eCommerce consultancy on a share capital sale and reinvestment

Capturing Capital: Succeeding in an Evolving Environment | TLT